The 10 Biggest Money Mistakes We See New Clients Make

Prospective Clients come to a Financial Professional for a variety of reasons. Typically, there is some sort of transition in the offing. Or, there is a pain point that has elevated to the point where they have to "talk to somebody". I thought listing a few of the more common areas in need of attention once a Prospect becomes a Client would be useful for you. Here they are...

1) No Umbrella Insurance

Umbrella Insurance is Property and Casualty Insurance jargon for “Excess Liability” Coverage.The intent of this form of insurance is to “step in” when your existing policy coverages reach the limit of their liability coverage. Then, the Umbrella Policy, which sits over your other policies as an umbrella would during a storm, takes over with a higher amount of liability coverage.

For individuals NOT seeking coverage for teenaged drivers, Umbrella Coverage is generally very affordable – usually between $300 - $500 per year for $1 Million of coverage. Generally speaking, no underwriting is required for coverage up to $3 Million, though this is dependent on the carrier. For completeness, teenaged drivers will drive premiums much higher.

Example:

- An example of when an Umbrella Policy comes into play is easy to construct – an automobile “accident”…my Driver’s Ed teacher in High School called them “wrecks”.

- Imagine inadvertently hitting a Vascular Surgeon in the prime of his career, who after colliding with you would never be able to perform another surgery for the rest of his life.

- Individuals usually carry somewhere around $500,000 of coverage on his/her auto policy.

- Well, it is somewhat to very unlikely the Vascular Surgeon will accept this amount for what was lost in the incident. This is where the excess liability (ie “Umbrella") coverage would come to the rescue.

- The policy usually includes legal fees and the services of the Insurance Company, who will negotiate on your behalf.

This snippet is not intended to be all-inclusive for what to know about Excess Liability Coverage. Conversely, the intent is to alert you to what risks you are assuming when in the course of your everyday activities. I recommend a call to your Property and Casualty Insurance provider for a quote – it’s easy and quick….believe me, they will know what you are talking about. Also, it is essential to know what is covered and what is not. For example, the Rent House for which you are the Land Lord is likely not covered. To put actual dollars to this, aClient to whom I recommended securing this coverage was quoted a rate of $17 per month. For about the price of a NetFlix subscription, you can buy yourself some peace of mind.

2) Incomplete or Non-Existent Estate Plan

Probably the most self-aware deficiency with which prospects come to Resilient Asset Management is an incomplete or non-existent Estate Plan. Meaning, most people know they need one, though for one reason or another, it’s not done.

For prospects who become Clients, addressing an incomplete Estate Plan becomes Item #1 on our list of “Things To Do” and it stays there until the Estate Documents are signed, notarized, scanned, and uploaded to Resilient’s online server for easy, fingertip retrieval.

For prospects who are single parents with minor children, we try to refer immediately and at times have “Zoom’ed” in an Estate Attorney to a prospect call. The reason is simple, for single parents with minor children, not having nominated a legal guardian via a properly executed Will throws the child into the arms of state law. While I am not an attorney, that just does not sound like something I would want to happen to any child.

So, do everyone in your life a favor and spend some time crafting an Estate Plan and then see it through to the cloud.

For an in-depth look at an Estate Plan Case Study, please see the following: ESTATE PLAN CASE STUDY

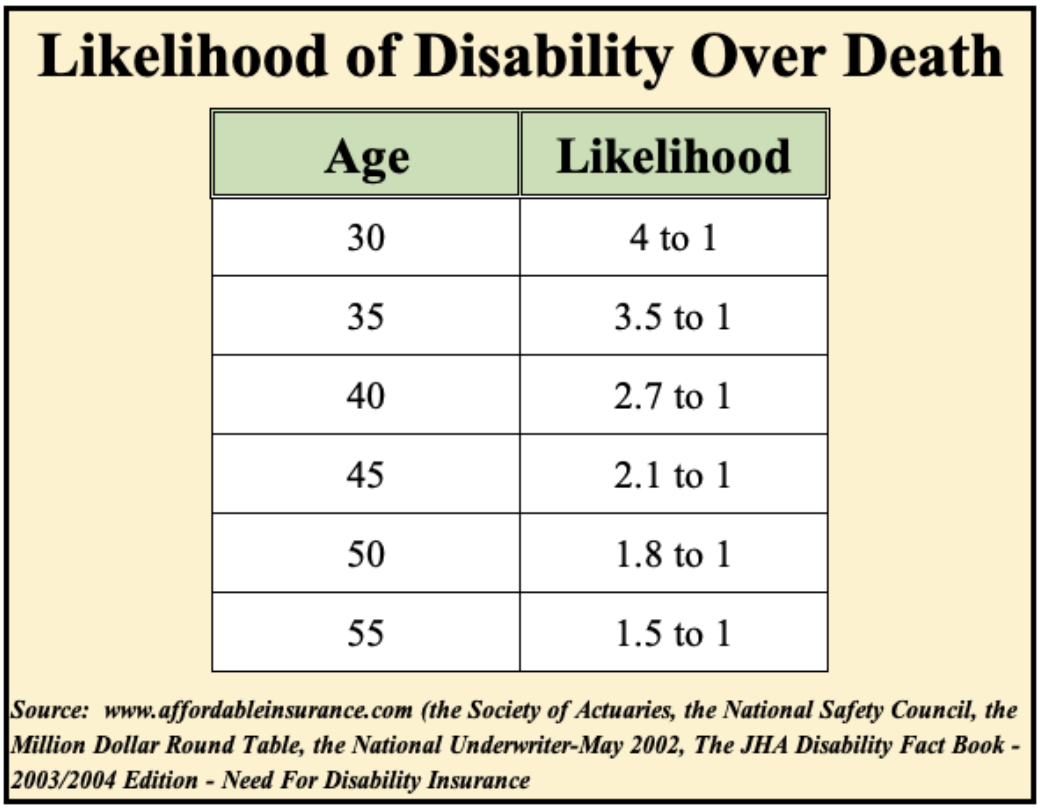

3) Ignoring Disability Insurance completely

For all people, the chances of becoming disabled – either permanently or temporarily – is greater than dying all the way into your late 60s. Here is a graph to illustrate that point:

And if you think about purely from a financial perspective, the worst thing that can happen in your life is a catastrophic event where you don’t die, though you can no longer work…of course, there are cascading effects to such an event.

Given the potential of such a calamity, it is very worthwhile to spend some time considering what would happen. For some, Disability Insurance is provided via an employer. For others – like Retired Military Retirees for example – they have pensions and VA Disability payments upon which to rely. Though for a large set of others not in either of these categories – think independent contractors and small business owners – Disability Insurance is a very real risk.

In summary, if you have not considered what would happen to you and your family in the event of your disability, I strongly recommend it.

4) Inadequate Life Insurance for each Individual in a Marriage

When couples consider Life Insurance, it is usually the primary earner whose income they seek to insure. This is an incomplete exercise, especially if one spouse works inside the home caring for young children. If this working spouse were to unexpectedly pass away, the same caring would have to be done, and it is unlikely the spouse working outside the home can come anywhere near doing the same job. Therefore, the spouse working inside the home probably needs life insurance coverage just as much as the spouse working outside the home.

For an in-depth look at estimating your life insurance needs, please see the following: ESTIMATING LIFE INSURANCE NEEDS

5) Inefficient Asset Location

Investments fall in three broad buckets:

- Taxable,

- Tax-Deferred

- Tax-Free.

How and when assets efficiently move into and out of each bucket is both art and science requiring a set of assumptions, various calculations, projections, and a plan. In today’s “No Fee” Trading and Minuscule Investment Expense world, this is a place where a Holistic Financial Planner can be invaluable.

A very common example of where this type of planning is appropriate is for military retirees with both a large Military Pension coupled with a large Thrift Savings Plan (TSP) balance. How this individual navigates distributions from the TSP along with a Social Security Claiming and Medicare decisions can have radically different outcomes based on what decisions are made. This is a prime area for Financial Planning assistance.

For some additional information on things to consider with asset location, please see the following:

- What To Do with your TSP funds when you leave military service

- Social Security for the Military Retiree

6) Making Poor Social Security Claiming Decisions

Claiming Social Security is a life altering financial decision. It used to be that you could monkey around with different strategies, undo claiming, and even make a restricted application. Now, the rules are much more strict and for practical purposes, it is difficult to un-pull the lever.

Additionally, probably the most misunderstood concept I witness amongst those considering claiming Social Security is how powerful deferring can be. These days, financial guarantees – from someone else – are very hard to come by. Well, the 7-8% increases you receive in annual payments when you defer Social Security is one such guarantee. Therefore, before you pull the lever on Social Security, you may want to talk to a Financial Professional.

7) Not paying Veterans Administration (VA) Disability Rating Application enough attention

For prospective Military Retirees, the VA Disability application is arguably one of the more important financial endeavors related to your retirement. I say arguably to cover my bases….to me, it is the most important claim one makes prior to retirement. The VA Disability system is a shadow retirement plan for which one qualifies as a consequence of his/her military service. Arguments can be made about the process and rating system itself. However, the bottom line is that potentially thousands of dollars of monthly Income Tax-Free money are at stake, so it is more than worthwhile to pay special attention to your VA Disability Claim.

Fortunately, there are many resources at your disposal – many of which are free. And in many cases, you get much more than you pay for, especially when you utilize a Veteran Service Organization (VSO) to assist with your claim, and perhaps, your appeal. And there are also many attorneys who will take cases on contingency should your rating adjudication not be to your liking.

For an in-depth look at VA Disability Claims, please see the following: ALL ABOUT YOUR VA DISABILITY CLAIM

8) Not having a professional review your Survivor Benefit Plan (SBP) Application

For prospective Military Retirees, the Survivor Benefit Plan is one of many topics covered on a full slate of Retirement-related topics during one’s Transition Class. In my view, this topic is poorly covered in most classes. Moreover, the applications are not properly reviewed when they are submitted.

The Survivor Benefit Plan (SBP) Application is one where you really, really, want to get it right the first time. If it is done properly, easy day – your coverage is organized the way you want right out of the retirement gate.

Conversely, if you make a mistake or want to change your election based on new information not fully understood during your transition class, changes require the intervention of the Service’s Survivor Benefit Plan Expert and the Defense Finance and Accounting Service (DFAS). Your application goes on “the pile”…today’s (January 2021) wait time at DFAS is 90 days.

Fortunately, my last job in the Navy was at Navy Casualty and I personally know the individuals who both teach the SBP Course in the Navy’s Transition Class and process SBP Applications. It is well-worth having these individuals review your application. This is not one you want to postpone or count on a redo.

For an in-depth look at the Survivor Benefit Plan, please see the following: THE SURVIVOR BENEFIT PLAN

9) Not fully appreciating the absolute power of systematic savings

For as much as ANY Financial Planner can do for you, systematic savings’ lies only behind “Making unwise financial decisions” in value. Simply put, the surest and most reliable way to grow your ending “retirement nest egg” is to save more. True, investment selection and performance, and the associated fees are important. However, the input with the largest impact – about 70% - is how much you save into the account.

Simply put, save until it hurts, and then perhaps, save a little more.

For a case study on the power of systematic savings, please see the following: ACTUALLY STAYING THE COURSE

10) Not taking advantage of the Back Door Roth IRA Contribution

A Roth IRA, under today’s Income Tax Code, is the best place for money to be. Again, according to today’s tax law, the money will never be taxed again for the remainder of your life. We won’t talk about after your life – that is another topic.

How money arrives in a Roth IRA is also a subject for much debate. That said, if you have exhausted all retirement account opportunities AND you have more cash to spare, a Back Door Roth IRA is an outstanding option. A simple example is a high-earning individual over 50, like a Military Retiree with a lucrative second career. She is optimizing her 401(k) Plan through work and still has cash to spare. Easy day, it is January 2021, so make a non-deductible contribution to a Traditional IRA for 2020 and 2021 for $7,000 each. Then, convert the funds to a Roth IRA, and BOOM, you have $14,000 in tax-free money. Wash, rinse, repeat year in and year out…over the long-term, great things are very likely to happen.

That's it - 10 areas I've had individuals and couples come to me over the years where I believe I have delivered significant value. Of course, there are other areas as everyone's situation is unique. If you would like to discuss your personal situation Schedule a 30-minute introductory meeting or contact us at chris@resilientam.com or (901) 318-3423.

About Christopher

Christopher Flis is founder and financial planner at Resilient Asset Management, a fee-only Registered Investment Advisor (RIA) based in Tennessee. Chris graduated from the United States Naval Academy with a bachelor’s degree in computer science, earned a Master of Science in Computer Science from the University of Minnesota, and attended flight school in Pensacola, FL, launching a fulfilling and distinguished military career. Chris spent 20 years in the Navy as an F/A-18 Strike Fighter Pilot, which included tours in Japan, Australia, and California, combat missions in all areas of the Persian Gulf and Afghanistan, and time spent as the Executive Officer of Naval Base Guam and Director of Navy Casualty in Millington, TN. When Christopher was ready to make a career change, he turned to a passion he held since high school when he attended a lecture on personal finance and started managing his own investments. He earned his Certified Financial PlannerTM (CFP®) designation and now combines his passions and experience by serving military, retired military, business owners, and retirees. Chris provides comprehensive, customized financial services, helping his clients overcome their challenges and take opportunities so they can achieve financial independence.

Chris lives in Downtown Memphis with his wife, Christine, and his son, Emerson. He is an avid runner and when he is not jogging for exercise, he is usually chasing his son around or walking his 3 dogs. To learn more about Chris, connect with him on LinkedIn.